May 11, 2024 • 6 min read • Market News

What lies ahead for the U.S. economy next year? While all predictions should be taken with a grain of salt, some economists have given their best shot using what we know today. Two prominent financial firms, Apollo Group, known for alternative investment management and Goldman Sachs, known for global investment banking and management, have shared opposing economic forecasts for 2024. Here’s how they compare.

Goldman Sachs’ View

Goldman Sachs shared an optimistic view for 2024, predicting only a 15% chance of a recession in 2024. The firm cites the following expected tailwinds to support their thesis of a strong 2024:

- Disinflation: core inflation should fall to 2%-2.5% by end of 2024

- Strong real household income growth due to a strong labor market

- Recovery in manufacturing after a subdued 2023 pace

- Increased chance of rate cuts if growth slows

While Goldman Sachs does cite possible headwinds, including a) further geopolitical risk in the Middle East and b) continued downward surprises to global manufacturing business surveys, it is their stance that there are more catalysts for improving the economy versus deterring it.

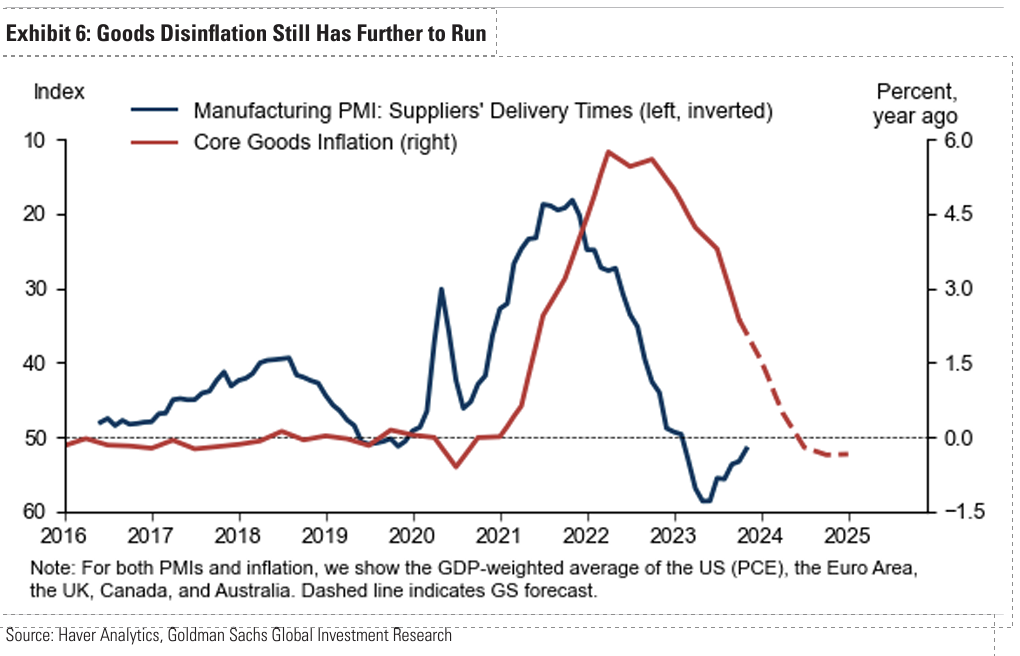

Analysts at Goldman Sachs believe that disinflation has further room to run, namely in core goods and shelter. The chart below displays a lag between manufacturing suppliers’ delivery times (blue) and core goods inflation (red). The dotted line displays the forecast expectation of core goods inflation.

Apollo Groups’ View

On the contrary, Apollo Group expresses a more grim forecast for 2024, citing upside risks to inflation and downside risks to growth.

Without linking a “recession-chance” percentage, Apollo's view coddles pessimism. Apollo Group expects rates to remain higher for longer due to a culmination of a) still-tight monetary policy, b) higher borrowing needs by the Treasury, c) loosening of yield-curve control in Japan, and d) reduced buying and holding of U.S. debt held by China.

To support its thesis of a likely recession, Apollo cites:

- Consumer spending threats: households running out of excess cash

- Student loan repayments commencing this past October, eating up an average of 7.5% of consumers’ monthly gross income

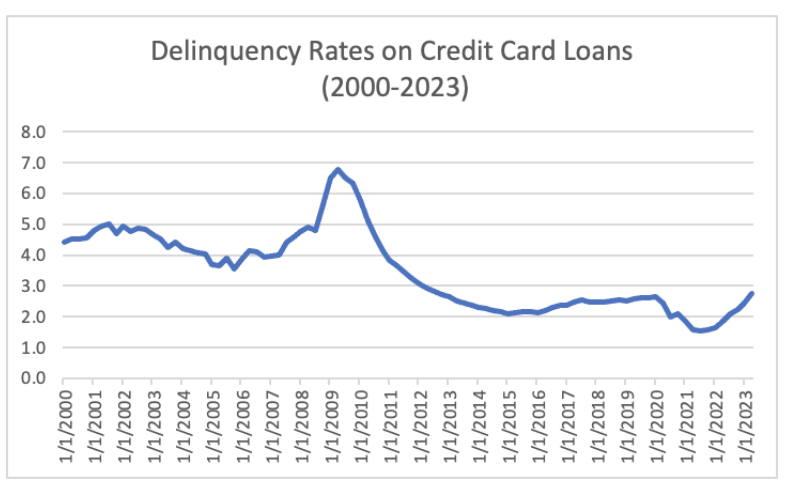

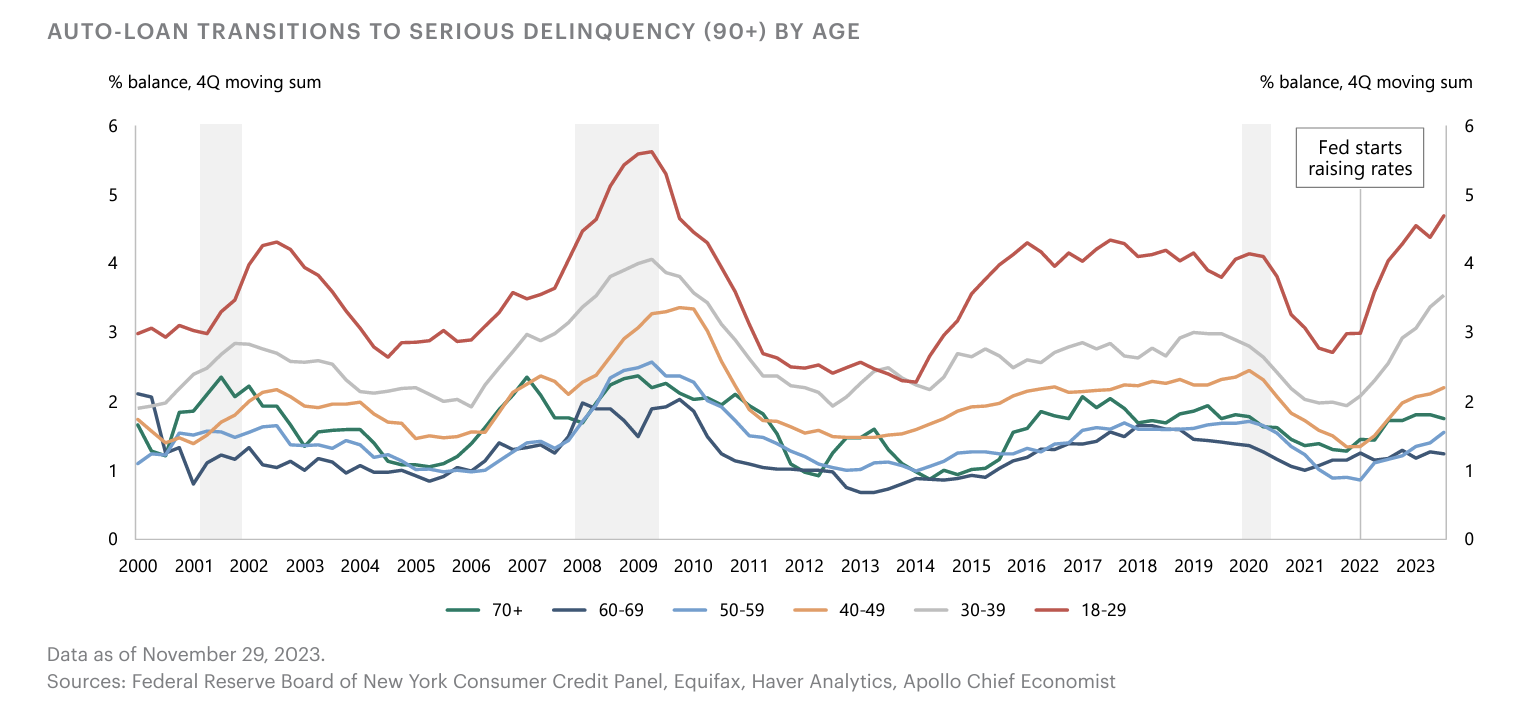

- Increased delinquencies in both credit-card and auto loans

- Employment beginning to soften

- Bank loan growth slowing sharply

- Decline in interest rate coverage ratios

- Markets not forecasting effect of higher rates on growth businesses with negative cash flow

For years, the Bank of Japan (BoJ) has supported the Japanese bond market by buying government debt to cap yields and keep local borrowing costs low. Recent actions to tighten its monetary policy and loosen its yield-curve control can push Japanese investors to move out of U.S. treasuries and back into the Japanese market. Japan is the largest international holder of U.S. treasury securities. Apollo believes that lessening international demand coupled with increased issuance of treasuries may increase yields, keeping rates higher for longer. Treasury auction sizes in 2024 are expected to increase ~23% across the yield curve (source: SIFMA, Haver analytics).

Our Take

We believe 2024 will be a year of tepid growth.

While both firms, Apollo and Goldman Sachs, provide strong references for their individual views, some of the supporting data can be misconstrued. For example, Yieldwink addressed credit card delinquencies (a supporting note made by Apollo) in our October Newsletter. While credit card delinquencies are moving higher, they are still well below their long-term average delinquency rates.

Source: FRED

Auto loan delinquencies, however, have pushed higher, particularly with the age groups of 18-29 and 30-39. We do not view auto loan delinquency as highly alarming in today’s market, namely due to its hierarchical priority in consumers’ needs. Extended work-from-home policies may have played a significant role in higher delinquencies.

Regarding Apollo’s comments on sharply declining bank loan growth, U.S. bank lending is considered a lagging indicator. In the Great Financial Crisis (GFC), bank lending bottomed out 12 months after the S&P 500. Apollo’s use of decreasing bank loan growth is not suggestive of a falling economy, as a decreasing growth rate is not synonymous with negative growth. In fact, loans and leases in bank credit have been growing while business loan delinquency rates remain near all-time lows.

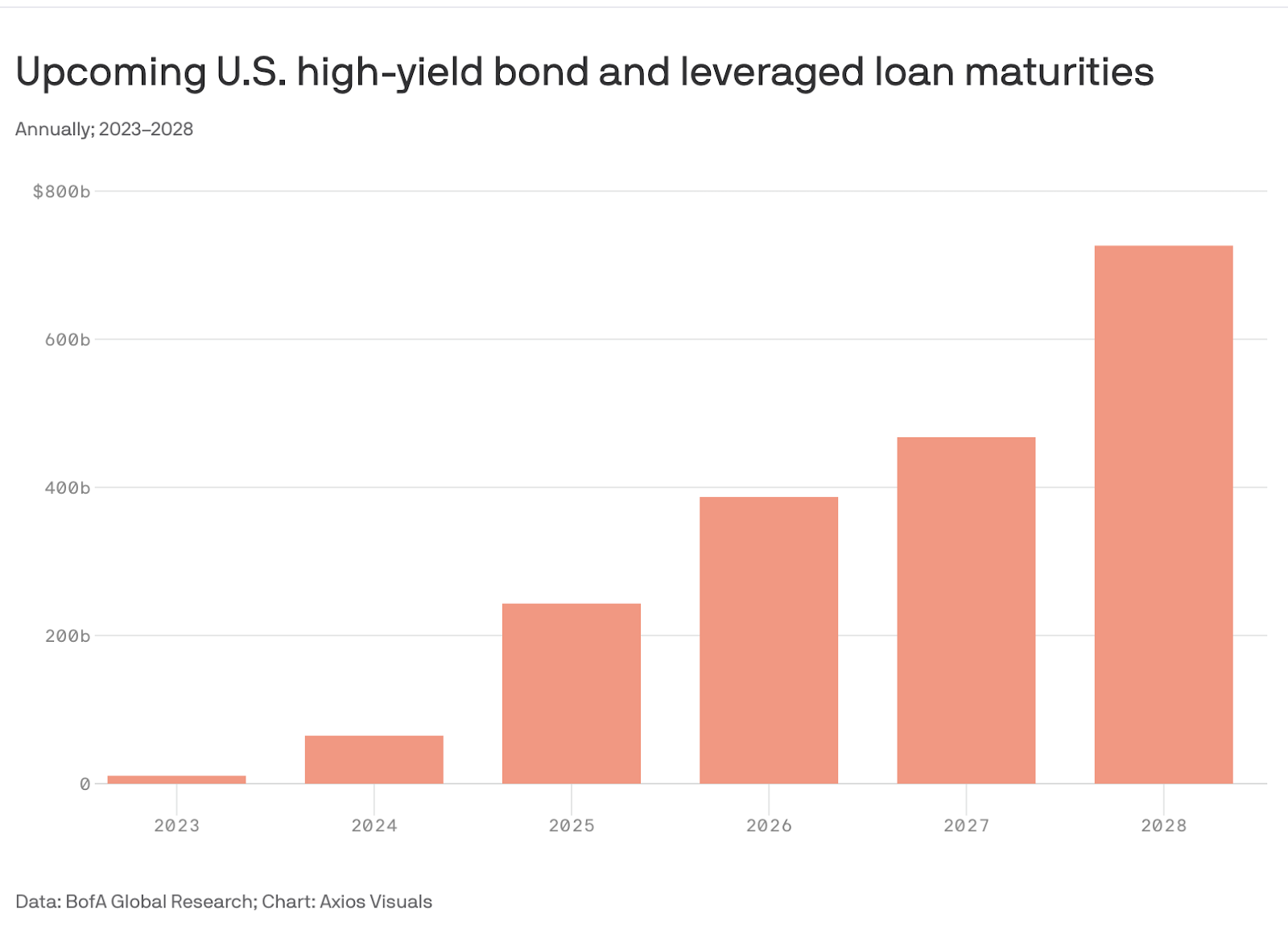

Should rates remain higher for longer, company defaults may take center stage. According to Bank of America Global Research, over $200B is to be refinanced in loan maturities in 2025. On average, companies start reviewing refinancing options 1.5 years in advance. Higher rates may make it difficult, if not impossible, for companies to refinance their debt at maturity. Defaults and/or bankruptcy will lead to higher job losses.

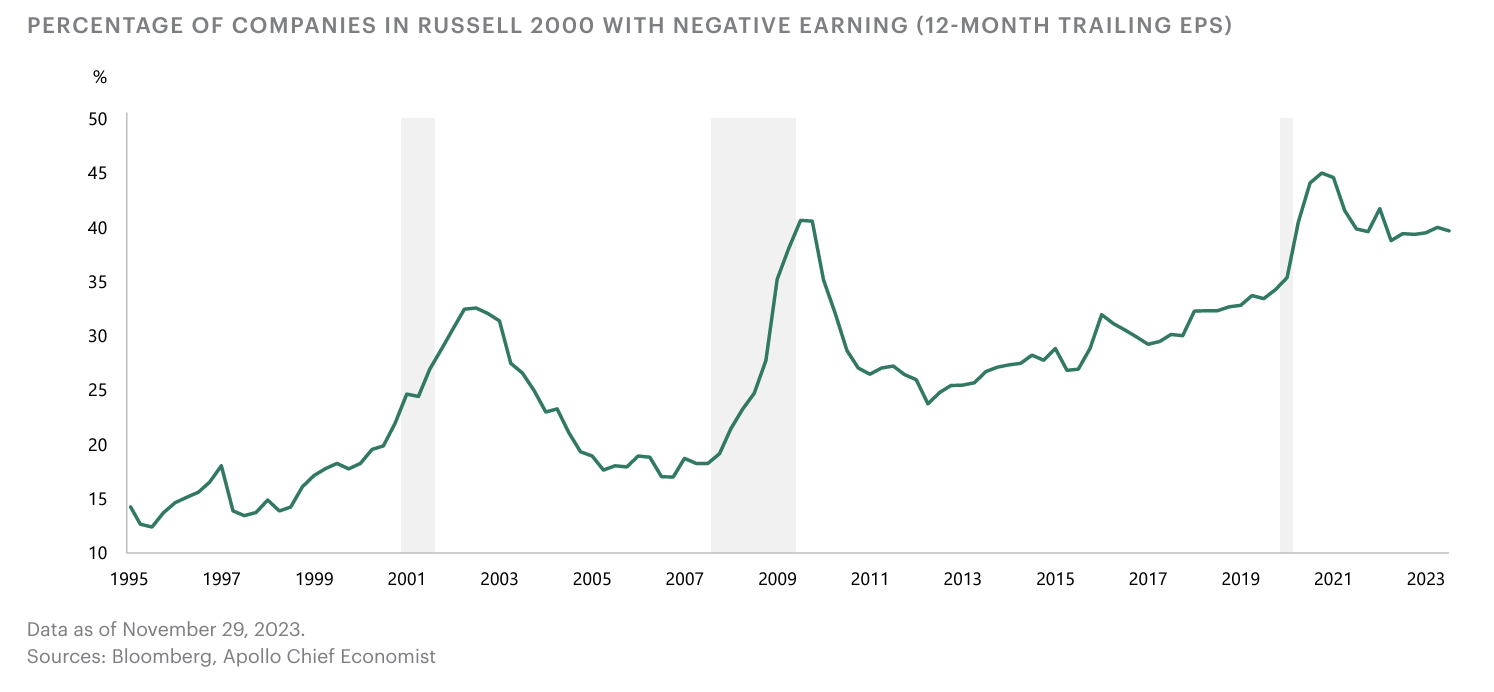

A surprising statistic: nearly 50% of companies in the Russell 2000 index have negative trailing 12-month earnings.

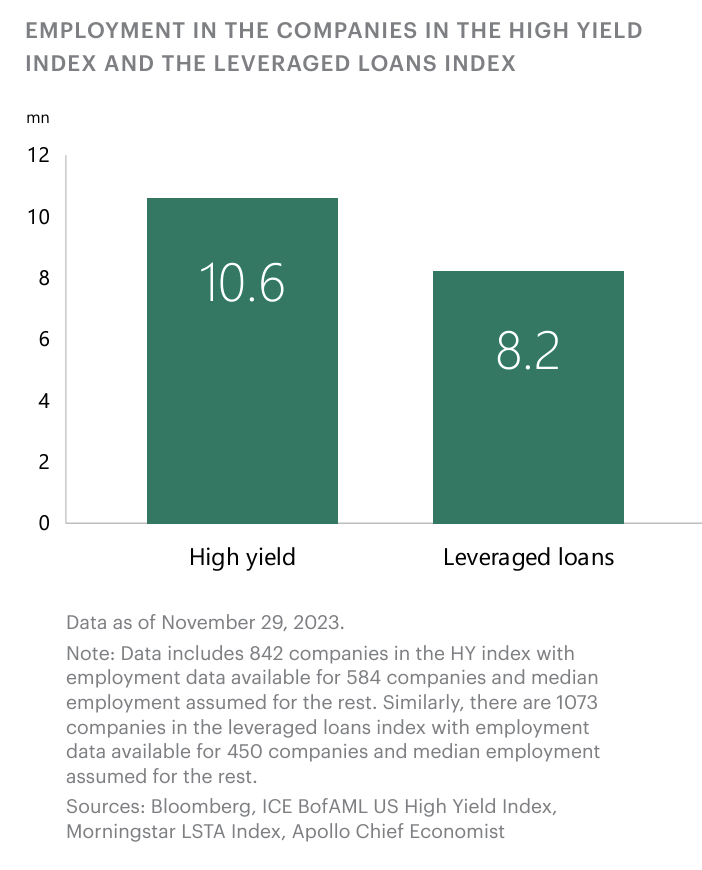

According to S&P Global, speculative grade corporate debt defaults are expected to reach 5% (86 defaults) by September 2024. The high yield and leveraged loan markets make up over 20,000,000 U.S. jobs.

Outside of the bond market, smaller bank balance sheets are another major concern as commercial loans, specifically loans made to office locations, come due with lower valuations.

While each view can make a compelling case, forecasts are just that — forecasts. All sides would agree that a well-balanced portfolio is warranted to help weather market volatility.

Enjoy the read? Sign up for our newsletter at the top of this page.

Make sure to follow us on:

Yieldwink is a digital platform linking investors to highly vetted private investments in an effort to lower volatility, provide higher levels of income, and enhance returns.

Yieldwink

Yieldwink