May 12, 2024 • 3 min read • Market News

Recent headlines from the Washington Post raised concerns about the American consumer, citing higher delinquencies on credit card and auto loans. The impact of higher interest rates on households (credit card interest and mortgage rates) have also been covered in the media.

We explored these concerns individually and examined their validity.

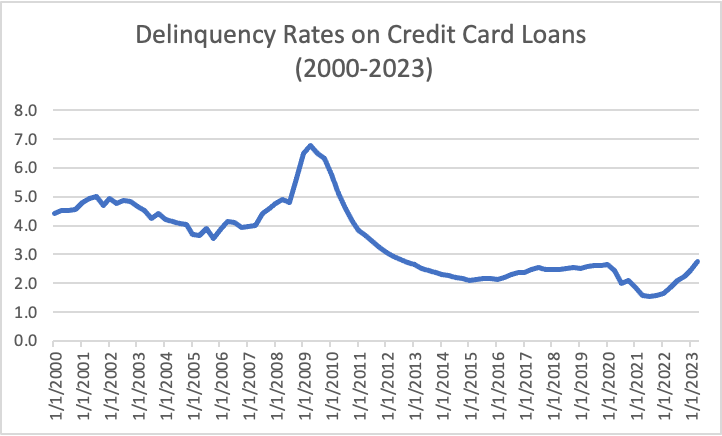

In a recent report, Wolfe Research’s analyst, Bill Carcache, examines credit-card delinquency rates among a few credit card issuers: Capital One, Discover, Synchrony Financial, and Bread Financial. Bill’s research shows that while credit-card delinquencies have increased year-over-year, they have shown signs of leveling off from their peak in Q1 of 2023. Credit-card delinquencies are higher today than a year ago, however, they are still well below historic averages (chart 1).

Chart 1 Source: FRED

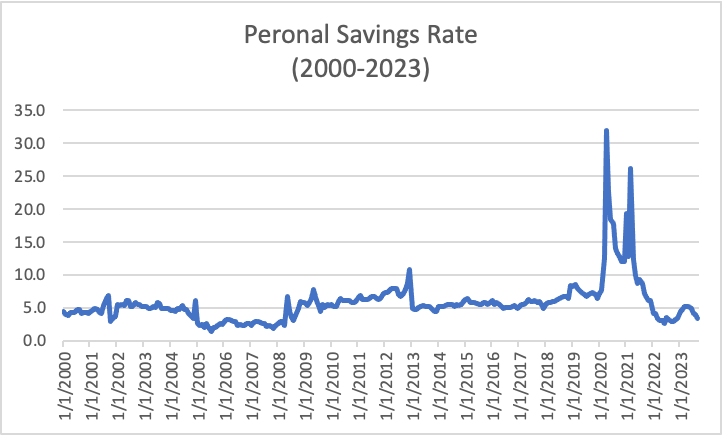

The personal savings rate (chart 2) for Americans has also dropped to its lowest level since the Great Financial Crisis of 2008. Americas’ savings rate has decreased from 7.2% in January 2020 (pre-Covid) to 3.4% as of September 2023.

Not all news is grim. Despite a lower savings rate, Americans still hold 10%-15% more cash in their bank accounts when compared to pre-COVID levels.

Chart 2 Source: FRED

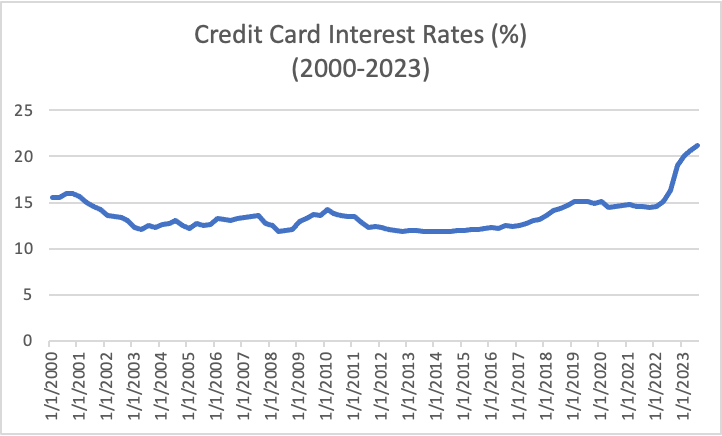

Credit card interest rates are up nearly five percentage points from early 2022 (chart 3). Higher credit card interest rates inhibit consumer savings on indebted households. For consumers with subprime credit (borrowers with low credit scores), the additional debt costs can place further strain on consumer pocketbooks.

Chart 3 Source: FRED

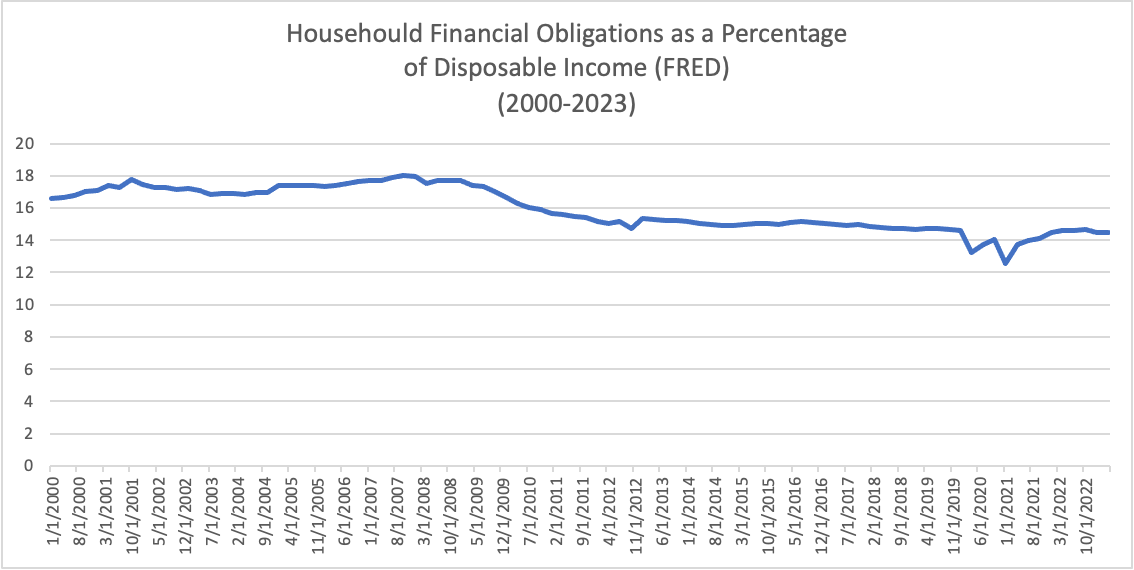

A recent J.P. Morgan report, however, estimates that debt servicing (or managing debt payments) has absorbed just 9.9% of household disposable income. That's still well below the 13.2% peak reached in 2008.

Household financial obligations as a percentage of disposable income (chart 4) tell the story of strength for the American consumer. “Household financial obligations” can be defined as consumer debt service payments plus housing costs as a percentage of disposable income. Refinancing to lower mortgage rates in the last decade has allowed Americans to save on debt expenses (mortgages), offsetting the effects of inflation on goods and services. According to the Federal Housing Finance Agency (FHFA), 91.8% of homeowners have a mortgage rate below 6%, with 62% of homeowners enjoying a mortgage rate below 4%.

Chart 4 Source: FRED

While new cautionary trends are emerging, we are finding that the American consumer currently remains resilient. Our team will continue monitoring specific leading and lagging economic indicators, including yield spreads. Since our June 2022 article, ‘Is the Economy Entering an Artificial Recession,’ 3-month and 5-year treasury yields have inverted — a historically fool-proof indicator of an impending recession. Consumer spending accounts for 68% of America's GDP, and will remain a closely watched predictor of the health of the American consumer.

Yieldwink

Yieldwink